Automobile theft is a demanding and irritating enjoy for any driving force. You might be wondering, Does car insurance cover car theft? The solution depends on the type of insurance you have. This guide will stroll you via the whole thing you want to know, from what kind of coverage you need to how claims paintings and what steps to take in case your vehicle is stolen.

Understanding Car Insurance Basics

Earlier than diving into whether or not or no longer car insurance covers car theft, it’s important to recognize the unique kinds of automobile insurance. The most common styles of insurance consist of legal responsibility, collision, and comprehensive insurance. Typically, this sort of typically consists of safety against robbery.

Whilst a person asks, does car insurance cover car theft? The short answer is sure; however, simplest when you have comprehensive insurance. Legal responsibility and collision insurance do not now encompass theft safety.

What’s complete coverage?

Comprehensive insurance is the coverage that solves the question: Does car insurance cover car theft with an affirmative answer? Comprehensive insurance protects you from damage caused by collisions. This includes robbery, vandalism, herbal disasters, fire, falling objects, or even animal harm.

So, if you’re involved approximately your car being stolen, you ought to without a doubt ask your insurer in case your present day plan includes comprehensive insurance. Without it, does car insurance cover car theft?? Probably not.

Example Scenario: Theft With and Without Comprehensive Coverage

Imagine rivers, Sarah and Mike. Sarah has comprehensive insurance, even as Mike has liability and collision coverage. One morning, each found out their motors were stolen. In Sarah’s case, her complete policy covers the loss. However, whilst Mike asks, Does car insurance cover car theft?—he finds out that his policy no longer does.

This state of affairs highlights the importance of having the right sort of coverage in case you’re worried about robbery. Surely, having automobile insurance isn’t sufficient if it does not consist of comprehensive coverage.

What Happens When Your Car Is Stolen?

Once your vehicle is long past, you’ll want to file a police report and declare with your insurance organization. One of the first things the insurer will ask is, Does car insurance cover car theft? Because the solution does vehicle coveragecoversr vehicle theft.

The insurance company will inspect the robbery and try to decide whether or not it’s a legitimate claim. This method may encompass reviewing security pictures, police statistics, and your very own account of the incident. The insurer makes use of these statistics to decide whether compensation is owed under the comprehensive policy.

How Much Will Insurance Pay for a Stolen Car?

Even though the answer to Does car insurance cover car theft is yes, that doesn’t imply you’ll routinely receive the entire fee of your automobile. Coverage corporations usually pay out the real cash value (ACV) of your car, not what you originally paid.

So, if your stolen car is 5 years old and has depreciated appreciably, your reimbursement will replicate that. When questioning Does car insurance cover car theft, keep in mind that coverage would not always imply complete financial restoration—particularly in case your vehicle has depreciated heavily.

Does Insurance Cover Items Stolen From Your Car?

A not unusual query tied to Does car insurance cover car theft is whether insurance also covers private belongings stolen from the car. Regrettably, vehicle coverage typically does not cover private objects like laptops, phones, or luggage stolen from within the vehicle.

If you need those items covered, you’ll need a homeowner’s or renter’s coverage policy. While the solution to Does car insurance cover car theft can be certain for the automobile, it’s generally notfor personal possessions.

What If Your Car Is Recovered After a Theft?

Occasionally, stolen automobiles are recovered weeks or months later. If this takes place after you’ve filed a claim and received a payout, the automobile now belongs to the insurance business enterprise. In this situation, does car insurance cover the car, nonetheless? Sure—but your possession rights may additionally switch to the insurer, relying on the terms of the claim settlement.

If the automobile is recovered before the claim is settled, the insurance organization can also, as an alternative, cover repair prices for any harm sustained during the theft. So even though the car is found, does car insurance cover car theft remain relevant because the insurer will, in all likelihood, pay for vital repairs?

Preventing Car Theft to Avoid Claims

Whilst it’s awesome to understand that the answer to Does car insurance cover car theft may be sure with the right coverage, it’s better to keep away from theft in the first place.. e Use anti-theft devices, park in well-lit areas, and constantly lock your automobile.

Taking those steps may also decrease your coverage premium. Insurers regularly deliver reductions for vehicles equipped with alarms or tracking systems. So, asking Does car insurance cover car theft ought to also be accompanied by way of how you can lessen the likelihood of needing to make a declare.

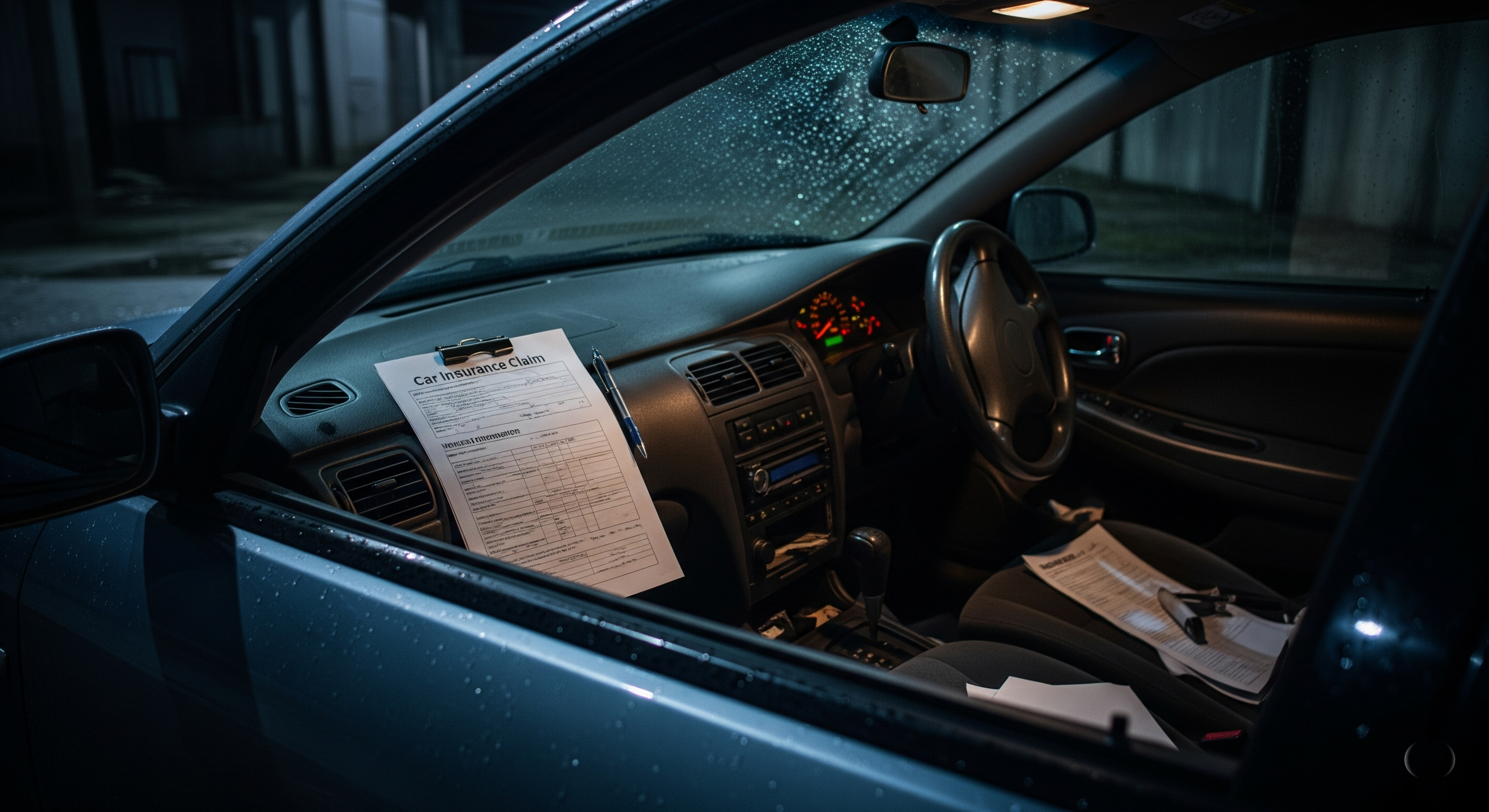

How to File a Theft Claim

As soon as you’ve confirmed that the answer to Does car insurance cover car theft is sure for your case, you’ll want to file a declare. Right here’s how:

- File the robbery with the police.

- Touch your insurer to report a claim.

- Offer important documents like the police document, automobile title, and any photographs.

- Cooperate with the insurance investigation.

- Await the insurer’s decision—they may provide a payout or wait to see if the automobile is recovered.

Understanding those steps is important if you’re looking to decide Does car insurance covers car theft and what the claims system will entail.

Does Leasing or Financing a Car Affect Theft Coverage?

If you’re leasing or financing a car, your lender may require comprehensive coverage. That’s because they have an economic interest in the automobile. In this situation, does Ddoescar insurance cover car theft? Issreater than a non-public concernnIt’ss a requirement agreement.

You can also be required to purchase hole insurance, which covers the distinction between what you owe on the auto and its real cost if it’s stolen. In this example, Does car insurance covers car theft remains certain, but gap insurance ensures you are not stuck with mortgage bills on a car you no longer own.

FAQs about car theft and insurance

Q1. Does vehicle insurance cover automobile theft if I left the keys inside?

Sure, even if you left the keys inside, does vehicle insurance cover vehicle robbery can nonetheless be spoken back, sure—if you have complete insurance. However, your insurer can also inspect for negligence, which can impact the claim.

Q2. Does liability coverage cover vehicle theft?

No, legal responsibility coverage does not. So if you’re asking, does vehicle insurance cowl car robbery and you simply have legal responsibility, the answer is any.

Q3. What if my stolen car is utilized in against the law?

If your vehicle is stolen and used in against the law, you gained’t be held responsible. Nonetheless, whilst asking does vehicle coverage cover car robbery, understand that your insurer may additionally want extra time to process the claim because of felony complications.

Q4. Does insurance cover vandalism if the auto isn’t stolen?

Sure, if you have complete insurance, it normally does. At the same time, as related, the query does car coverage cowl vehicle robbery isn’t like coverage for vandalism, but both are usually included under complete insurance.

Q5. Am I able to nevertheless get insurance after a car theft?

Yes, however, your top rate may grow. As soon as you’ve requested vehicle coverage, covered vehicle robbery, and filed a claim, insurers may also see you as a higher hazard.

Conclusion

To sum it up, the answer to Does car insurance cover car theft depends onyour insurance policy. Handiest complete coverage consists of robbery protection. Legal responsibility and collision coverage won’t help if your car is stolen. Ensure to check your cutting-edge plan and consider including complete insurance if theft is a concern.

Knowing the solution to Does car insurance cover car theft is essential for financial safety. Do not wait until it is too overdue—evaluate your coverage, improve your insurance if needed, and take preventive measures to defend your car nowadays.

Read More: Does Health Insurance Cover Car Accidents?